A recent story has surfaced after influencer and former teacher Mohd Fadli Salleh shared a post on Facebook regarding a woman’s concerns over a housing loan.

In an anonymous sharing, the woman explained that her husband had asked her to apply for a housing loan in her name, as it would be easier to secure approval due to her status as a government employee.

For illustration purposes only

Malaysians share their two cents

Netizens quickly flooded the comments section, with many appearing divided on the issue.

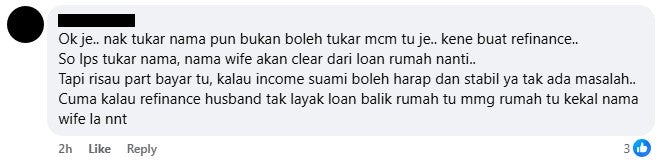

“I feel like this should be okay. If you want to change the name later, you can do it through refinancing. Once the name is changed, the wife’s name will be cleared from the housing loan. My only concern is about the payments; if the husband’s income is reliable and stable, there shouldn’t be a problem. But if he doesn’t handle the loan during refinancing, the house will remain in the wife’s name.”

“Just use the wife’s name. After all, the husband promised to pay, and providing for the wife is his responsibility. If she has the opportunity to take the loan, trust your husband. If he can’t pay at any point, he should still make an effort. Once you’re married, everything is shared. As long as the husband is able, he won’t neglect paying for the house. Worrying about divorce from the start is the wrong mindset; if you’re already thinking about divorce, maybe it’s better not to get married at all.”

“When you’re married, you get to know your spouse inside and out, including his finances and family background. If he can handle all household finances responsibly, including monthly maintenance for the children, and the wife hasn’t defaulted, then that’s a blessing. But if you’re sharing this concern on social media, it shows that you don’t fully understand or trust your husband. Trust is key to keeping a marriage strong until the hereafter. If you don’t feel confident, have an honest conversation with him. If you feel that your husband has never taken advantage of you and can support you during tough times, then I don’t see any problem.”

“If you’re borrowing under your name, you can’t just change it whenever you want, unless the loan is fully paid off within those two years. That’s wishful thinking; it’s better not to take the risk. You might get scammed without even realising it. If you really want, both names can be on the loan. That’s only fair. If things don’t work out, you can sell it together and split the proceeds.”

“Fadli has already warned you. It’s better not to change the loan to your husband’s name. Keep it under the borrower’s name because changing it is risky.”

“Don’t change the name so that you won’t have to worry about inheritance claims for his siblings or anything like that. If it’s in the wife’s name, just pay it off fully. There’s no need to transfer the name at all.”

What are your thoughts on this? Let us know in the comments!

Also read: “From Land Rover to RM1 Kancil” – M’sian Left with Debts & Lawsuits After Husband Abandons Her